Before reviewing performance in detail, it is important to contextualise the operating environment during the period under review. Sri Lanka entered the quarter on a solid footing, with GDP growth reaching 5.0% in calendar year 2025 (CY25), while Q4 CY25 recorded a 4.8% YoY expansion, sustaining two years of post-crisis recovery momentum.

Inflation increased by 2.2% YoY as of end-March, with core inflation rising due to higher transport, housing, electricity, gas, and fuel costs, reflecting the pass-through effects of global commodity price pressures following geopolitical tensions in the Middle East. On the monetary front, the weekly AWPLR rose by 34 basis points during the quarter, while market liquidity expanded.

Despite these external headwinds, private sector credit grew strongly by 27% YoY, driven in part by businesses building inventory to mitigate supply chain disruptions, and also reflecting continued confidence in the domestic economy. The Sri Lankan rupee depreciated by a further 2% against the US dollar during the quarter, bringing full-year depreciation to 5.6% in 2025. Gross official reserves improved to USD 7.0 Bn, supported by inflows from multilateral sources, further strengthening external sector stability.

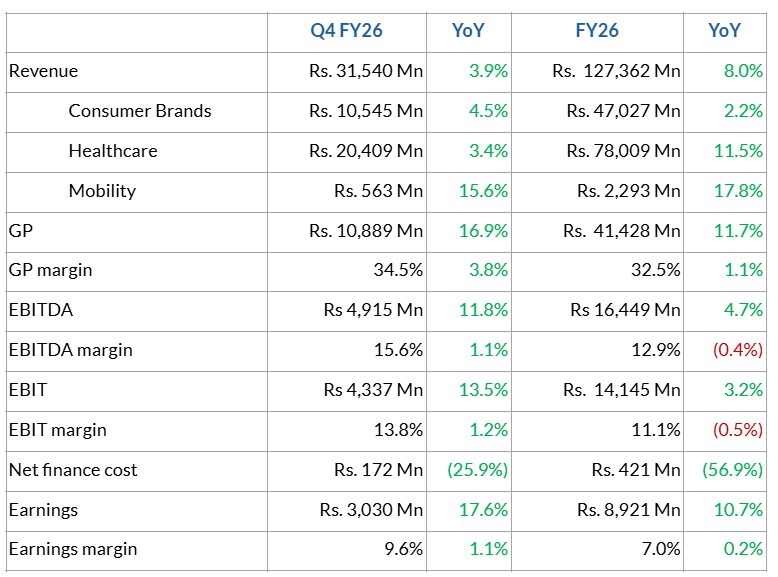

Group Performance in Detail

The commentary that follows focuses primarily on quarterly performance, as the FY26 Annual Report available on Hemas' Investor Relations page and the CSE website covers full year performance in detail across the CEO's Review, Group Strategy, and Sector Review sections.

Sector Performance

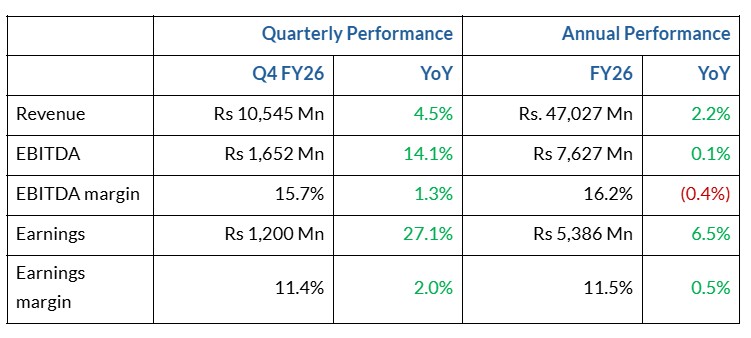

Consumer Brands

Consumer Brands delivered quarterly revenue growth of 4.5% YoY, with an outstanding earnings growth of 27% YoY.

The Sri Lankan Home and Personal Care industry delivered moderate year-on-year growth. Personal Care, which makes up approximately 45% of the local industry, was the strongest performer, recording double-digit growth of 13% in Q4 and 17% for the full year. Personal Wash and Home Care were broadly flat. Baby Care, spanning both Personal Care and Personal Wash, was the other double-digit growth category, recording 12% quarterly and 13% annually.

Hemas’ Home and Personal Care – Sri Lanka delivered strong quarterly growth of 16.6% YoY, with 97% of that growth volume-led, a compelling indicator of underlying demand. Personal Care, representing 61% of the portfolio, grew 16% YoY during the quarter. Beauty, a strategic priority within the Personal Care category, recorded growth of 19.5%, largely driven by volume expansion. Home Care recovered from its annual drag, recording 11.4% YoY expansion in Q4 driven by volumes. Some portfolio discontinuations also partially influenced the overall growth figure.

Personal Care and Beauty constitute the primary focus of the Group’s long-term growth strategy, while Home Care remains a conscious and considered element of the portfolio. Hemas will continue to lead the introduction of global consumer product trends into the local market, tailored with local insights. This value-added proposition will drive the Personal Care category forward, with new formats across several subcategories planned for launch in FY27.

Home and Personal Care – Bangladesh

The Value Added Hair Oil industry in Bangladesh recorded value growth of 3.9% year-to-date as of December 2025, although volumes declined over the same period.

Home and Personal Care – Bangladesh delivered revenue growth of 11% YoY in Q4 and 13% for the full year FY26. Earnings recorded an exceptional increase of over 140% YoY in FY26, although Q4 earnings declined YoY due to higher promotional activity during the period, but within budgeted expectations. Margins expanded, driven by an improved sales mix favouring higher-margin products, complemented by effective cost price controls.

Looking ahead, Home and Personal Care – Bangladesh will define its growth trajectory through new category development, leveraging its extensive distribution network to drive sustained profitability.

Learning

The school season shift resulted in revenue and volume contraction for Atlas Axillia in Q4 FY26 relative to Q4 FY25. However, the newer portfolio verticals Back to School and EduToys recorded significant volume growth during this period. The book, pen, and pencil categories also gained market share during the quarter. The next school-based seasonal uplift is expected in Q3 FY27; in the interim, focus will be directed toward developing the broader portfolio to sustain profitability.

Distribution optimisation is driving meaningful uptake of higher-value ranges, particularly within Back to School and EduToys, with early results encouraging. As a market leader in learning, Atlas continues to champion e-learning in Sri Lanka, leading the evolution toward technology-enabled educational experiences.

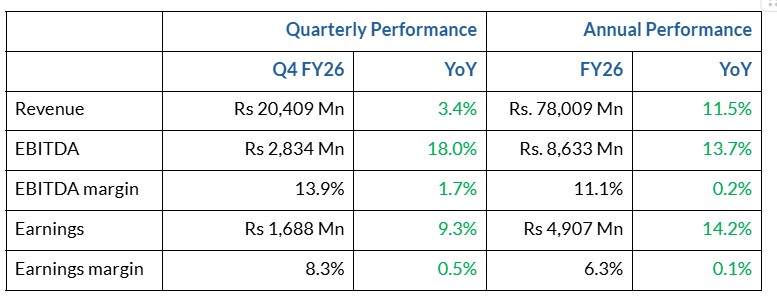

Healthcare

Revenue growth of 3.4% translated into earnings growth of 9.3% in Q4; a compelling demonstration of margin leverage in the Healthcare segment performance.

Pharmaceutical Distribution

The private pharmaceutical market in Sri Lanka grew by 6.7% in volume and 8.7% in value in the quarter ending December 2025. Hemas Pharma maintained its strong market leadership during the quarter.

Hemas Pharmaceuticals saw Q4 FY26 revenue broadly flat relative to Q4 FY25. While the quarter remained profitable, YoY earnings growth was marginally negative due to a higher tax charge in Q4 FY26. On a full-year basis, however, both revenue and earnings recorded YoY growth.

New product approvals during the quarter continue to support the pipeline for future periods. Distribution re-engineering and digitalisation are expected to drive further margin improvement, while the consumer wellness portfolio is being actively scaled as an additional profitability driver.

Pharmaceutical Manufacturing

For the twelve months to December 2025, the private pharmaceutical market recorded value growth of 9.6% YoY, volume growth of 8% YoY, and a market value of Rs. 113 Bn. Against this backdrop, Hemas’ pharmaceutical manufacturing arm, Morison, delivered a strong performance for the twelve months ending March 2026, achieving volume growth of 18.6% in pharmaceutical manufacturing.

Morison advanced its value market share ranking to #23 in the total private pharmaceutical market by end December 2025, gaining 14 positions from the previous year, while maintaining its volume market share at #2, reflecting continued broad-based growth across the business.

The business now generates 75% of its revenue from manufactured pharmaceuticals and OTC products, while the remainder is derived from diagnostics. In FY26, Morison discontinued its import and distribution of pharmaceuticals, transferring this function within the Group for improved focus and strategic alignment. Following the divestment of distributed pharma agencies, Morison recorded earnings growth in excess of 100% YoY in FY26 across its manufacturing and diagnostics portfolios.

As the first local manufacturer to introduce Empagliflozin, Cilnidipine, and Rivaroxaban in Sri Lanka—representing latest-generation therapies in diabetes and cardiology—Morison has redefined the capabilities of local pharmaceutical manufacturing. Within just two years of launch, the Empagliflozin brand EmpaMor has achieved a market-leading position in volumes, while the newer cardiology range, including CilniMor, BisoMor, and RivoMor, is gaining strong traction in the market.

Looking ahead, Morison is actively pursuing export opportunities, with EU-GMP certification currently underway—a significant milestone that will enable access to international markets.

Hospitals

Hemas Hospitals delivered revenue growth of 24% in FY26, driven by volume growth across all services. This momentum continued into Q4 FY26, with total admissions increasing year-on-year, supported by a 19% growth in surgical admissions. Over the first three quarters of FY26, Hemas Hospitals recorded revenue growth of 26%, significantly outpacing the listed hospital industry.

Looking ahead, the Liver Program’s growing caseload is emerging as a meaningful near-term driver of revenue and earnings, reflecting Hemas Hospitals’ broader push to scale capabilities across high-demand specialties. This clinical ambition is underpinned by a strategic focus on establishing Hemas Hospitals as a digitally mature, insight-driven healthcare brand. A key pillar of the Group’s long-term capital allocation and growth strategy, the Thalawathugoda facility expansion is progressing steadily. Groundbreaking has been completed, regulatory engagement is ongoing, and the facility is targeted to commence revenue contribution in 2029.

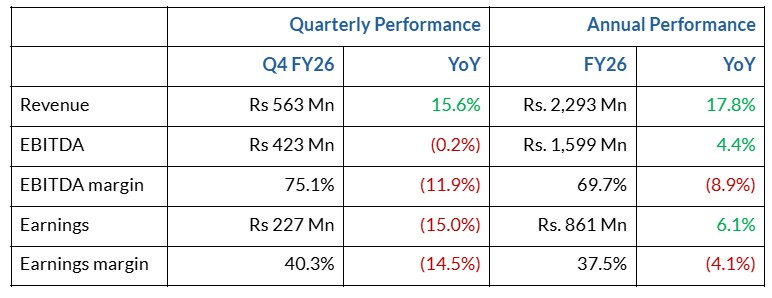

Mobility

Mobility delivered a strong performance with revenue growth in both Q4 and FY26, though Q4 earnings

were impacted by the Middle East crisis, which had an immediate and meaningful effect on the aviation

segment.

Within Maritime, Evergreen recorded exceptional Q4 TEU volume growth of 44% against an industry growth of 10%, reflecting both the strength of Hemas’ principal relationships and Colombo’s growing prominence as a regional transshipment hub.

Intensified competition and geopolitical disruptions, most notably the impact of the Middle East conflict on passenger volumes and network capacity toward the end of FY26, created a more challenging operating environment for Aviation. Forbes Air Services recorded a quarterly revenue decline of 17% YoY, although full-year earnings growth remained marginally positive. Emirates maintained its air cargo market leadership while ranking second in passenger market share across operated routes.

Mobility is well positioned to capitalise on the growth in regional trade and travel, supported by Sri Lanka’s increasing relevance as a neutral Indian Ocean logistics and maritime services hub, together with strong principal relationships that provide a platform for further expansion. Particular emphasis will be placed on expanding maritime support services, including ship spare logistics, crew logistics, and outer harbour services, to strengthen the core agency business, while also focusing on high-potential adjacencies in regional logistics to capture value from evolving regional trade dynamics and leverage Sri Lanka’s strategic positioning.

Sustainability

The Group continued to advance its sustainability agenda during the quarter, delivering steady progress across environmental priorities and social impact initiatives. These efforts support long-term resilience, regulatory readiness, and reinforce the Group’s position as a purpose-led organisation.

Cumulative plastic recovery surpassed 2.9 million kilograms, reflecting continued progress toward the Group’s commitments to recover 50% of plastic placed on the market by 2025 and 100% by 2030. This also positions the Group to meet upcoming Extended Producer Responsibility (EPR) requirements.

Water intensity increased marginally from 1.5m³ to 1.6m³ compared to Q4 FY25, highlighting the need for continued focus on operational efficiency. In response, targeted conservation and efficiency initiatives are being accelerated across key operations to mitigate resource risk, minimise potential cost escalation, and strengthen long-term water security.

Renewable energy adoption reached 11.1% of total electricity consumption, marking continued progress toward the Group’s target of 25% renewable energy usage. Additional opportunities are being pursued to optimise energy sourcing, improve cost stability, and reduce carbon exposure over the medium term.

The Group continued to generate meaningful social impact across education, health and wellbeing, and inclusion, reaching over 28,900 individuals during the quarter. These initiatives strengthen community engagement and support the Group’s social license to operate within the communities in which it operates.

Sustainability priorities continue to be embedded into business decision-making and operational performance across sectors, with near-term focus areas including accelerating renewable energy adoption, improving water efficiency in high-risk locations, and scaling post-consumer waste recovery efforts to meet 2030 commitments.

Strategy and Outlook

Post quarter, inflation rose further to 5.4% in April as commodity price increases filtered through the economy, driven primarily by higher transportation and housing, water, electricity, and fuel costs. While the Middle East conflict is expected to exert pressure on the balance of payments through higher fuel import costs and softer tourism receipts, continued growth in remittances, bilateral and multilateral inflows, together with anticipated IMF disbursements, are expected to provide meaningful buffers and moderate the overall impact on the Sri Lankan economy. Periodic price increases across the portfolio are anticipated as commodity cost and exchange rate pressures continue to transmit to consumer prices.

Importantly, Sri Lanka’s recent crisis experience has strengthened institutional and corporate resilience, and Hemas is no exception. The Group enters FY27 stronger, sharper, and well positioned for growth. The FY30 Long Range Plan, anchored around USD 100 Mn in investments over the next four years, outlines an ambitious growth trajectory, with internationalisation and adjacency expansion serving as its two defining strategic themes. The Group is also actively exploring entry into an additional business vertical during this period, further broadening its platform for long-term value creation.

Ashish Chandra

Group CEO

May 22, 2026

Colombo