Hemas Holdings PLC (HHL) delivered resilient results in the first six months of the financial year 2023/24

to post a cumulative Group revenue of Rs. 59.0 billion, a 13.5 per cent growth over previous year. Amidst

the increasing strain on operating expenses, the Group's operating profit and earnings for the period

experienced a marginal growth of 4.1 percent and 3.7 percent, reaching Rs. 4.9 billion and Rs. 2.3 billion,

respectively.

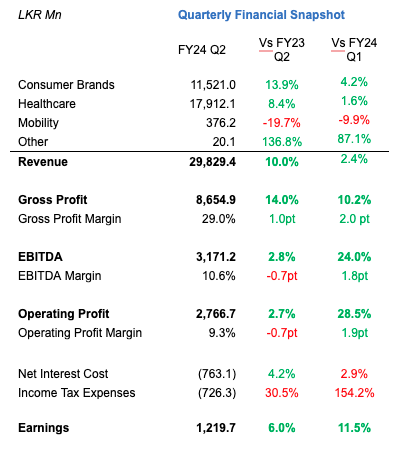

During the quarter, the Group achieved a 10.0 percent growth in revenue, posting Rs.

29.8 billion for the quarter, with operating profits and earnings for the quarter

increasing to Rs. 2.8 billion and Rs. 1.2 billion, respectively.

Operating Environment

In comparison to the previous year, Sri Lanka's economic landscape has shown some developments.

There has been a significant reduction in inflation with September closing at 0.8% growth on a

year-on-year basis although being on an inflated base. Amidst ongoing pressure on the external

sector, the exchange rate remained fairly steady throughout the quarter, and interest rates experienced

a substantial decline of over 120 percentage points, reducing the burden associated with financing costs.

Given the progress made in the domestic debt optimisation efforts and external debt restructuring discussions,

the disbursement of the second tranche of the IMF loan is anticipated in the near future.

Nevertheless, Sri Lanka continues to face a multitude of issues, including elevated unemployment rates,

constrained disposable income of individuals, and the formidable challenge of managing an extensive debt burden.

Consumers, grappling with reduced purchasing power, maintained a cautious approach to their spending patterns.

Consumer Brands

Contrary to anticipations, the market's performance during the quarter fell short of expectations.

Many key product categories experienced volume contractions on a year-on-year basis, while consumption

was stagnant compared to the previous quarter. The heightened utility prices had a pronounced effect on

consumer spending, affecting the offtake in both modern and general trade channels. This situation was

exacerbated by adverse weather conditions, which further impacted consumer income and foot fall to outlets.

The stationery market continued to become increasingly competitive, with all market participants gaining ground through

improved range availability and aggressive price competition. Amidst the increasing pressure on consumer spending power,

the market witnessed many new entrants in the value-for-money segments where a high traction was observed.

Despite the Government's efforts to provide essential food items to low-income communities at subsidised rates, inflation

in Bangladesh persisted, exceeding 9 per cent, and disproportionately impacting the underprivileged communities. Amidst

the strained economic environment, the trend of consumers shifting towards more affordable alternatives continued into the

quarter under discussion, causing a decline in the hair oil market.

The cumulative revenue reported for the Consumer Brands Sector witnessed a growth of 19.9 per cent to reach Rs. 22.6 billion

while the operating profits reported a growth of 37.0 per cent due to reduced raw material prices, improved productivity and

stable exchange rates. In line with the growth in operating profits and lower finance costs earnings for the period witnessed

a growth of 74.9 per cent to reach Rs. 2.0 billion.

The Sector reported a revenue of Rs.11.5 billion for the quarter, a growth of 13.9 per cent over last year driven by the performance

of both the Home and Personal care and Learning Segments. The earnings improved by 67.3 per cent to surpass the Rs 1.0 billion mark

due to over 50 per cent reduction in finance cost under improved working capital base, along with reduction in key raw material prices.

Home and Personal Care

Despite the decline in the overall industry demand, the company augmented its market presence, bolstering its outreach through the

addition of over 5,000 outlets during the period, and fulfilling consumer needs. Prices were maintained in line with the market,

while strengthening the value prepositions to secure higher market share in key segments, notably within the domains of baby care

and feminine hygiene. With the expansions via pharmacy and beauty channels, revenue from the beauty segment under the ‘Prasara’ and

‘Vivya’ brands experienced significant growth during the quarter. 'Prasara' also introduced its latest addition to its comprehensive

total solution portfolio, the body purifying tonic, during the quarter. The business continued to invest in multiple efficiency

improvement and supply chain optimisation initiatives with a view of improving agility and consumer centricity.

‘Baby Cheramy’ was recognised as the "Best Baby Care Brand" in the 'Retail Category' at the prestigious Global Brand Awards 2023,

a reflection of Baby Cheramy’s unwavering position as the undisputed market leader in the country.

Learning Segment

Despite the heightened competition in the market, the Learning Segment effectively maintained its leading market

position with volume-led growth. In response to the evolving consumer preference for value-driven choices,

the Learning Segment extended its ‘Homerun’ stationery line by incorporating books into the product portfolio,

providing an accessible and cost-effective range for consumers.

Consumer Brands International

Despite ongoing challenges stemming from the increasing strain on disposable incomes and a demanding economic environment, the business in Bangladesh demonstrated notable resilience, achieving double-digit volume-led growth. Expanding on the recent launch of the cost-effective 'Kumarika 150 ml' variant, the business further diversified its product portfolio by entering the pure coconut hair oil market with the introduction of 'Kolombo,' a product tailored to cater to this specific segment.

The heightened emphasis on expanding the export portfolio within the Home and Personal Care and Learning segments has consistently advanced, with noteworthy developments such as the introduction of ‘Kumarika’ featuring a specialised SKU, ‘Kumarika Cooling Oil’, in the Middle East. Furthermore, there has been substantial advancements in the realm of Original Design Manufacturing, particularly in specific regions within East Africa.

Healthcare

The healthcare landscape continued to face heightened difficulties, including shortages of medicines and migration of doctors and other healthcare workers, which placed considerable strain on the healthcare ecosystem. Disruptions in the regulatory and procurement processes of the Government healthcare system led to the public having limited access to quality medications and medical care. The double-digit contraction witnessed in the preceding quarter in the private market eased in the quarter under discussion mainly due to the traction in essential categories. Profit margins remained under pressure due to price reductions mandated by the National Medicine Regulatory Authority (NMRA) to align with the exchange rate of Rs. 295 per dollar, with no subsequent adjustments made to account for adverse movements in exchange rates. Industry stakeholders are persistently advocating for a transparent pricing mechanism that accurately reflects the cost structure in a timely manner.

The cumulative revenue for the Sector increased by 10.4 per cent to reach Rs. 35.6 billion driven by the Pharmaceutical Businesses of the Group. While the sector's operating profits of Rs 2.7 billion increased by 6.3 per cent in line with revenue growth, this upward momentum was not translated into earnings, primarily due to escalating finance costs related to funding working capital in the Pharmaceutical Busiensses.

The Sector posted a revenue of Rs. 17.9 billion for the quarter, a growth of 8.4 per cent over last year, while the operating profits increased by 16.0 per cent to Rs. 1.6 billion. However, the benefit was negated under heightened finance costs, to report an earnings growth of 6.0 per cent.

Pharmaceuticals

The Pharmaceutical Distribution Business introduced 22 new products into the market in both pharmaceutical and surgical segments. New launches were made in the much-needed spaces including diabetes and cancer related medication. The business actively pursued various initiatives aimed at optimising its working capital position, resulting in a significant reduction in the working capital base compared to the last financial year.

In line with its vision to make premium healthcare affordable, the Pharmaceutical Manufacturing Arm of the Group, continued to focus on Morison branded portfolio posting over 70 per cent volume growth for the period, driven by the success of several recent product launches. During the quarter, Morison ventured into third party manufacturing by producing Sitagliptin, a medication used in the treatment of type 2 diabetes, on behalf of a prominent global player. ‘Homagama' factory crossed the 50 per cent capacity utilisation primarily as a result of its allocation for fulfilling Government orders.

Hospitals

Revenue from key anchor specialties including Nephrology, Cardiology and Gastro-Enterology continued to witness double digit growth for the period. Despite a decline in surgical admissions, the Hospitals Business sustained its overall occupancy levels at both facilities, surpassing 55 percent under improved medical admissions.

Mobility

The Maritime Sector continued to face challenges as both import and export activities to and from the country encountered the effects of a global economic slowdown. However, there has been relative improvements under eased import restrictions and growing momentum of merchandise exports. Stemming from lower base from the previous year, the Port of Colombo observed a notable upturn, with transshipment and total throughput volumes registering growth of 9.5 per cent and 7.7 per cent respectively.

Aviation Industry witnessed relative improvements on a quarter-on-quarter basis in both the cargo and passenger segments. The growth in cargo was supported by the relative improvements in exports, while the passenger sector benefited from increased business and student traffic.

The Mobility Sector posted a cumulative revenue of Rs 787.0 million, a decline of 13.8 per cent in comparison to the same period last year while the earnings witnessed a higher decline of 53.9 per cent mainly due to the reduced finance income for the Sector. Accordingly, the quarter witnessed a decline of 19.7 per cent and 59.9 per cent to reach Rs 376.2 million in revenue and Rs.136.8 million in earnings under challenging operating conditions.

Leading with ESG

The Group remained dedicated to addressing plastic pollution by promoting responsible plastic waste management and supporting the national Extended Producer Responsibility (EPR) initiative. Partnering with Eco Spindle, the Group established two baling sites in Ampara and Colombo, ensuring the responsible disposal of over 350,000 kg of plastic annually.

During the quarter, the Group continued efforts to empower families for aspire for a better tomorrow. Through its Feed a Future initiative, conducted in partnership with Hoppers London, 1,097 protein packs were distributed to children and families across 33 ‘Piyawara’ preschools in 11 districts. The 63rd ‘Piyawara’ Pre School was added to the national network, benefiting 50 children from underserved communities in Kegalle. The Group created quality education experiences and equal learning opportunities to over 74,000 children, teachers, and parents. The Group's initiatives to tackle period poverty involved educating 12,000 Sri Lankan women on menstrual health, and over 3,000 diabetes tests were conducted to raise awareness and assist in the early management of diabetes in communities.

Outlook

While Sri Lanka's economy displays certain signs of recovery, with moderating inflation, stabilized exchange rates, and efforts to rebuild reserves, the broader macroeconomic and policy landscape continues to present formidable constraints. Challenges persist in terms of consumer sentiments and constraints on disposable income will continue to pose obstacles for businesses across the industries.

Hemas maintains a cautious yet optimistic outlook, drawing upon its expertise to ensure resilience as the country navigates the complexities of the economic recovery phase. The Group's strategic objectives remain closely aligned with its purpose, propelling innovative solutions to address the continually evolving consumer landscape.

In our forward-looking approach, Hemas will continue to grow in Consumer and Healthcare spaces while greater emphasis is placed on the development of core capabilities of localised innovation, internationalisation, and the establishment of a distinctive Sri Lankan pharmaceutical brand. Moreover, the Group is focused on simplifying its operations in order to enhance efficiency and agility.

Kasturi C. Wilson

Group Chief Executive Officer

November 09, 2023

Colombo